Markets Dawn Europe: Wed 8 by 7AM UKT (8AM CET)

Brief Podcast 🎙 + Data 📊 + Script 📄

Script: Estimated reading time ⏲ ~5 mins

Good morning,

European equities closed at record highs yesterday on strong earnings by banks and traders’ optimism over sooner-than-later central bank action. The Stoxx 600 gained 1.14%, its second-best day this year to a record high as did the FTSE 100 after advancing 1.22%. The best-performing European stock markets so far this year are Ireland, the Netherlands, Italy and Germany, with gains between 10 and 15%.

Wall Street ended almost unchanged with Disney dropping nearly 10% after reporting poor updates on its conventional TV business and weaker cinema box office.

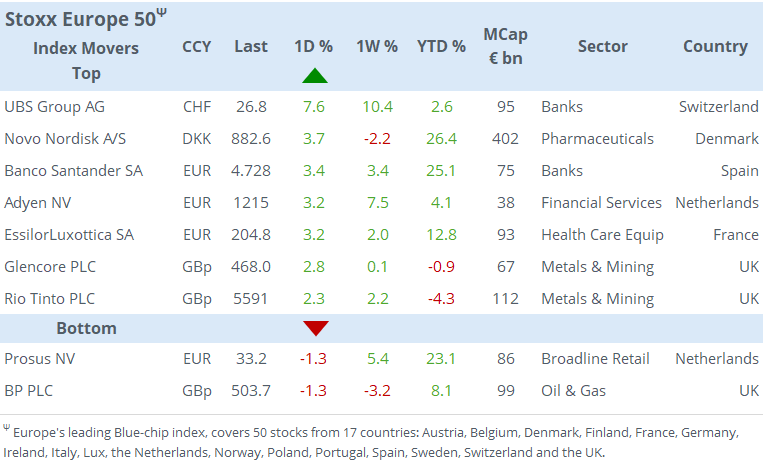

In European earnings, UBS surprised with its first quarterly profits ($1.8bn) since rescuing Credit Suisse sending shares up by 7.6%, its best day in 13 months for a total market cap of $94bn. UBS’s wealth management unit reported $27bn in net new assets and the bank maintained its share buyback plan for the next three years.

Another mover was German chip maker Infineon Technologies gaining 13% after reporting better-than-expected revenues (€3.6bn) in a challenging environment. Infineon is valued at €47bn.

Saudi oil giant Aramco reported a 14% drop in quarterly profits of $27bn and declared a $31bn dividend. Shares were unchanged yesterday and are 10% lower YTD for a market cap of $1.9tn. It is 82% owned by the Saudi government and expects to pay out $124bn in total dividends this year.

€-zone retail sales rebounded sharply in March, +0.8% MoM and +0.7% YoY, reversing the previous month’s weakness and significantly above estimates.

German industrial orders surprisingly fell in March and February was revised lower to reflect a drop. Manufacturing output declined again in March, further accentuating Germany’s economic underperformance in the €-block.

Dutch inflation printed at 2.7% YoY in April, down from 3.1% a month earlier.

Minneapolis Fed President Kashkari made hawkish remarks regarding a potential rate cut and suggested that borrowing costs may need to be held on hold for an extended period, possibly all year, to bring inflation down to target. He suggested that actual data does not reflect a convincing disinflation process.

Bond market action was centered in Europe with Bunds and Gilts prices advancing as both yield curves shifted lower by 6 to 10bp. 10-year Gilts closed at 4.13% and Bunds at 2.42%. In forex markets, cable was the notable mover with a nearly 0.5% fall to 1.2504, as traders position for a dovish Bank of England at tomorrow’s policy meeting.

Asian equities are dropping today with Tokyo and Singapore down by more than 1%. The Bank of Japan warned of potential policy action if the weakening of the yen impacts prices. The currency reversed its recent recovery and is dropping again, now trading above 155. Toyota reported an ~80% profit increase on strong sales and a weaker yen.

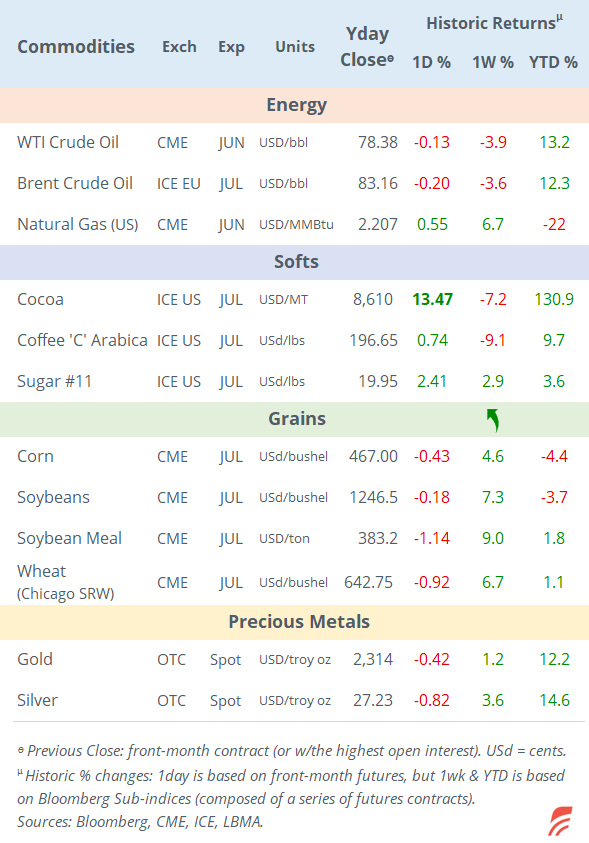

European futures are mixed; the FTSE is marginally firmer while the Eurostoxx 50 is slightly weaker. Bund futures are also trading lower this morning. Crude oil is lower, down 0.5% to $82.70 and Bitcoin is steady at $62,500.

Data updates today include industrial output in Germany, Spain and Denmark, retail sales in Italy and Sweden’s central bank will hold its policy meeting at 8:30 London time. Analysts expect a 25bp rate cut to 3.75%. Tonight, Brazil’s central bank meets with the Selic rate expected to be cut to 10.50%.

Companies reporting results today include BMW, Inbev, Ahold, Munich Re, Alstom, Uber and Airbnb, among others.

Copyright © 2024 Laconic. All rights reserved. This publication, 'Markets Dawn Europe,' contains proprietary content and is intended solely for the recipient's personal use. Please share the publication using the button below, as access is free to all.