Markets Dawn Europe: Wed 3 Jul

Podcast 🎙 Data 📊 Script 📄

Good morning,

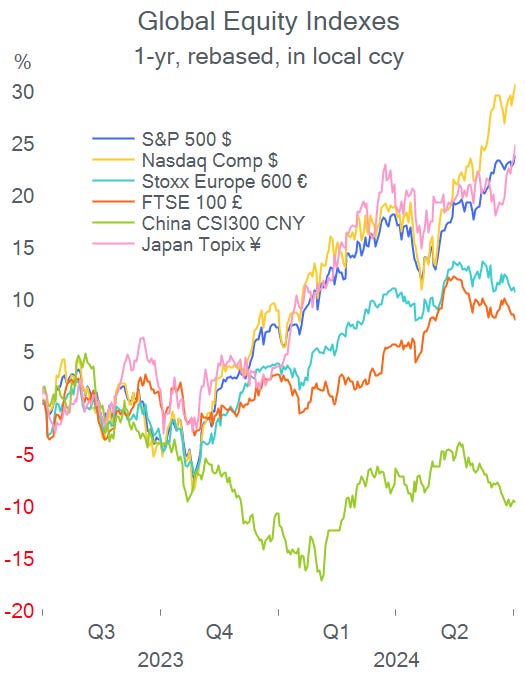

Stocks in Asia are rising today with Hong Kong, Singapore and Taiwan up by more than 1%, mainly on the back of Powell’s somewhat dovish comments yday. The ¥ is weaker again as it nears 162. European equity futures are firmer in early morning trading (€-Stoxx50 +0.5%) while bond futures are flat after benchmark yields fell a few basis points yday following Monday’s sell-off.

Wall Street closed higher last night driven by another positive session for growth stocks and a steep rebound for Tesla. European markets remain volatile ahead of the UK’s general election tomorrow and France’s legislative elections on Sunday. Madrid’s Ibex index was the clear underperformer, down 1.3% with Santander (-2.8%) as the weakest Stoxx 50 index member.

In data, €-zone headline inflation eased to 2.5% YoY in June from 2.6% a month earlier. ECB’s Lagarde said that inflation is heading in the right direction and was very advanced in the disinflationary path despite Services inflation remaining high. She projected the €-zone headline inflation to be closer to 2% in the next 12 months. Markets are pricing in one ECB rate cut in September (66%) and a high chance (90%) of another before year-end.

Fed’s Powell confirmed that the US economy is on a disinflationary path after making significant progress but that even more data is required to cut rates as the central bank balances price pressure and employment goals.

Headlines:

-Biden is facing increasing pressure from the Democratic party to withdraw from the race following the poor debate which he attributed to jet lag. State governors requested a meeting with Biden’s team to discuss his candidacy as Trump maintains a clear lead in the polls.

-French centrist and left parties withdraw candidates from Sunday’s run-off election to try and stop Le Pen’s National Rally from obtaining a majority.

-Beryl, the earliest ever Cat 5 hurricane now downgraded to 4, heads towards Jamaica and the Caymans today after devastating smaller islands around Grenada. Advancing at 35 km/h, it is expected to hit Mexico’s Yucatan peninsula on Friday.

-Hungarian PM Viktor Orban, EU’s most pro-Putin leader, made his first visit to Ukraine since the invasion. He encouraged Zelensky to set a deadline for a ceasefire agreement with Moscow. Hungary is the only EU member to oppose Brussels' military aid to Ukraine.

Tesla’s vehicle deliveries in Q2 declined for a second consecutive quarter to 444k units, -15% QoQ (-4.7% YoY) but marginally less than analysts' expectations. It is the first time that deliveries have fallen for two straight quarters. However, Tesla maintained the electric vehicle crown above China’s BYD (mcap $92bn) which delivered 426k in Q2 (+21% YoY). Tesla (mcap $737bn, P/E 59x) shares rallied 10% to a six-month high (-7% YTD).

In debt capital markets, Chile placed a 7-yr sovereign bond in €, rated A2/A, at mid-swaps+105bp.

In credit ratings, Sony Group (Japan, mcap $105bn) was upgraded one notch by Moody’s to A2.

Data to be released today include PPI in the €-zone; Service PMIs in most developed countries; international trade, jobless claims, ADP employment and factory orders in the US. Also, Poland’s central bank meets today (unch at 5.75% exp) and the Fed’s last meeting minutes will be released.

Constellation Brands (US, mcap $47bn), the brewery behind the Corona and Modelo brands will report earnings before markets in NY open.

Remember that US exchanges will close at midday ahead of tomorrow’s holiday. Britain holds its general election tomorrow. On Friday, non-farm payrolls for June will be the main economic update. Markets Dawn Europe will take a two-day break and return on Monday. Happy 4th of July to our American audience.

See you soon.

Copyright © 2024 Laconic. All rights reserved. This publication, 'Markets Dawn Europe,' contains proprietary content and is intended solely for the recipient's personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.