Markets Dawn Europe: Wed 26 Jun

Podcast 🎙 Data 📊 Script 📄

Good morning,

Wall Street ended firmer last night with growth stocks outperforming value names as the Nasdaq 100 added more than 1% while the Dow Jones Industrials dropped almost 0.8%. Nvidia recovered partially after rallying 7%.

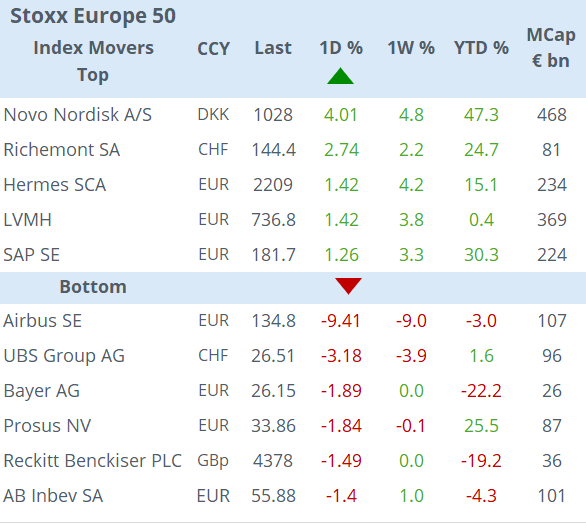

Europe finished weaker with Airbus (mcap €107bn) as the driver of negative sentiment after it issued a profit warning due to complications in the engine supply chain. Shares plunged more than 9%, its worst day in almost 3 years to a seven-month low, pulling the aerospace and defence sector lower. Airbus reports results in late July.

On a positive note, Europe’s largest company, Danish pharma Novo Nordisk (mcap €468bn) was the best performer among Stoxx 50 members, adding 4% to an all-time high and helping Denmark’s OMX index advance 2.7% on the day and 29% YTD. The catalyst was the approval in China of its weight-loss drug Wegovy.

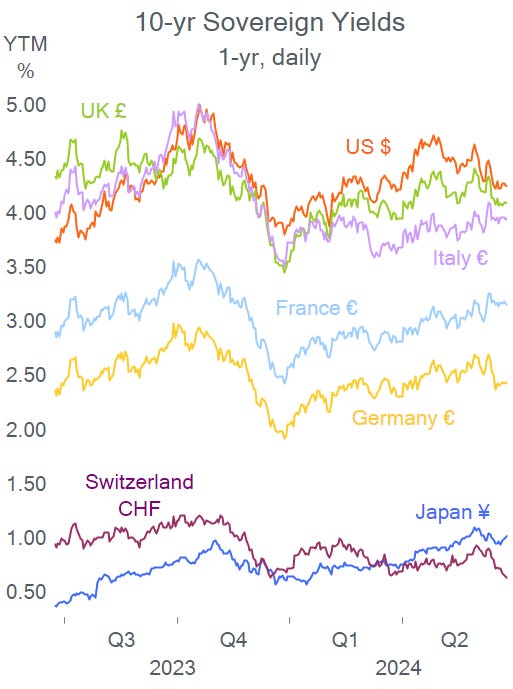

It was another quiet day on the bond market front with benchmark yields barely moving ahead of Friday’s US inflation update. US treasury yields remain at 4.24%, Bunds at 2.41% and Gilts at 4.08%. Currency markets were also little changed with the focus on a potential intervention of the Bank of Japan if the yen continues to depreciate.

Asian markets are mixed today with Australian stocks dropping 0.7% and the Aussie dollar is appreciating 0.5% following the inflation update. Australia reported a higher-than-expected inflation of 4.0% YoY, accelerating from 3.6% a month ago, mostly on higher housing and transport prices. Equity benchmarks in Japan, Korea and Taiwan are trading firmer while mainland China is a touch weaker.

In Europe, the €Stoxx 50 and Dax futures are firmer by around 0.5% in early trading. Brent oil is now above $85 again following a weak session across all commodities yesterday.

Headlines,

-It was Microsoft’s turn to be charged with breaching EU antitrust law yesterday. Brussels is accusing it of gaining an unfair advantage by bundling the communications Teams app with its Office suite of software products to the detriment of competitors such as Zoom and Slack. Microsoft (mcap $3.35tn) shares we little changed and it remains the world's largest company.

-Denmark will implement a carbon tax on farmers for each cow they own, the first such measure in agriculture. Livestock farmers will pay €16 per tonne of carbon dioxide equivalent emission per cow, roughly €100 per animal. The methane produced by cows accounts for around 7% of global greenhouse emissions.

-Fed speakers were active yday sending mixed signals. FOMC voting Governor Michelle Bowman, said she remained willing to raise interest rates again should inflation stop declining or increase. She sees upside risks to inflation such as an aggressive fiscal stimulus.

Another voting member, Lisa Cook, expects inflation to ease more notably next year and that eventually the Fed will need to cut rates. Futures markets are pricing in just a 10% chance for a Fed rate cut in late July, a 66% chance for a cut at the September meeting and a 46% chance of two rate cuts this year.

In corporate deals, Australia’s Macquarie Group (mcap $50bn) will divest its 40% stake in Italian energy company Hydro Dolomiti Energia for around €1bn.

Volkswagen will inject up to $5bn into US electric vehicle maker Rivian Automotive (mcap $12bn) sending shares 50% higher in after-hours trading. At yesterday’s closing price, Rivian shares had declined 50% this year.

In equity capital markets, footwear company Birkenstock Holding Plc (UK and Nasdaq-listed, mcap $11bn), shares fell more than 4% after leading shareholder L Catterton sold 14mn shares in a secondary offering worth >$800mn. Birkenstock was listed last October and was trading at a record high before the transaction.

There are no significant data releases scheduled for today besides US housing figures.

That’s all for today, see you tomorrow.

Copyright © 2024 Laconic. All rights reserved. This publication, 'Markets Dawn Europe,' contains proprietary content and is intended solely for the recipient's personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.