Markets Dawn Europe: Wed 17 by 7AM UKT (8AM CET)

Brief Podcast + Data + Script

Podcast ↑↑↑↑ Scroll down for the script.

Good morning,

We’ll begin with today’s headlines:

Israel is still considering how to respond to Tehran’s air attack while the US announced it plans economic sanctions on Iran. Tensions in the Middle East became the latest driver of market sentiment.

Russian forces continue to advance into Eastern Ukraine as they push locals to abandon cities in the Donetsk region.

The IMF has upgraded its forecast for US GDP growth for this year to 2.7%, double the pace of its G7 counterparts, while Germany will be the weakest with a 0.2% annual expansion. UK growth is seen at 0.5% and the €-zone at 0.8%. The Fund predicts US inflation for 2024 at 2.9% and the €-zone’s at 2.4%. The estimates reflect the US economic dominance and could mean the Fed easing cycle could take longer.

Markets in the US ended marginally lower last night as yields continued to climb. Jerome Powell made hawkish remarks, saying that recent inflation updates have not provided the Fed enough confidence to cut rates in the short term, suggesting that policy interest rates will remain high for longer.

On the other hand, ECB policymakers insisted on their plan to cut rates in June if the disinflation trend continues. Morgan Stanley and Deutsche Bank see a total of 75 bp reduction of the deposit rate this year.

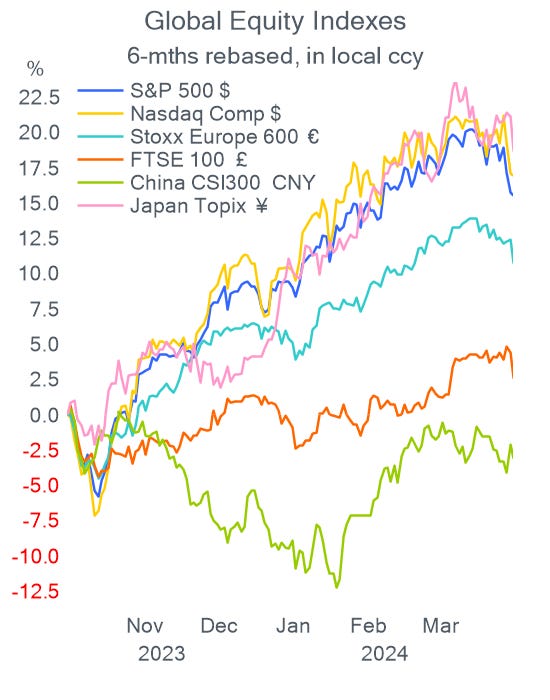

European equities dropped sharply as they priced in the previous day's sell-off in the US. It was the region's worst day in nine months. Every sector and country benchmark ended lower with basic resources (-3.1%) and banks (-2.6%) as the weakest. The FTSE 100 lost 1.8% and the broad Stoxx 600 fell by 1.5%.

In earnings updates, Europe’s second-largest company, LVMH, reported its weakest quarterly revenue growth in 3 years (+3% organically to €20.7bn) mostly on lower demand from Chinese consumers. Shares dropped 1.6% yesterday and remain 6.6% higher this year, for a total market cap of €392bn.

In the US, both Bank of America (-3.5%) and Morgan Stanley (+2.5%) beat Q1 revenue and profit estimates but Bank of America shares dropped on the back of higher loan loss provisions. Tesla shares fell nearly 8% in the past two days, to the lowest level in one year, after announcing a global workforce reduction of 10% due to increased Chinese competition.

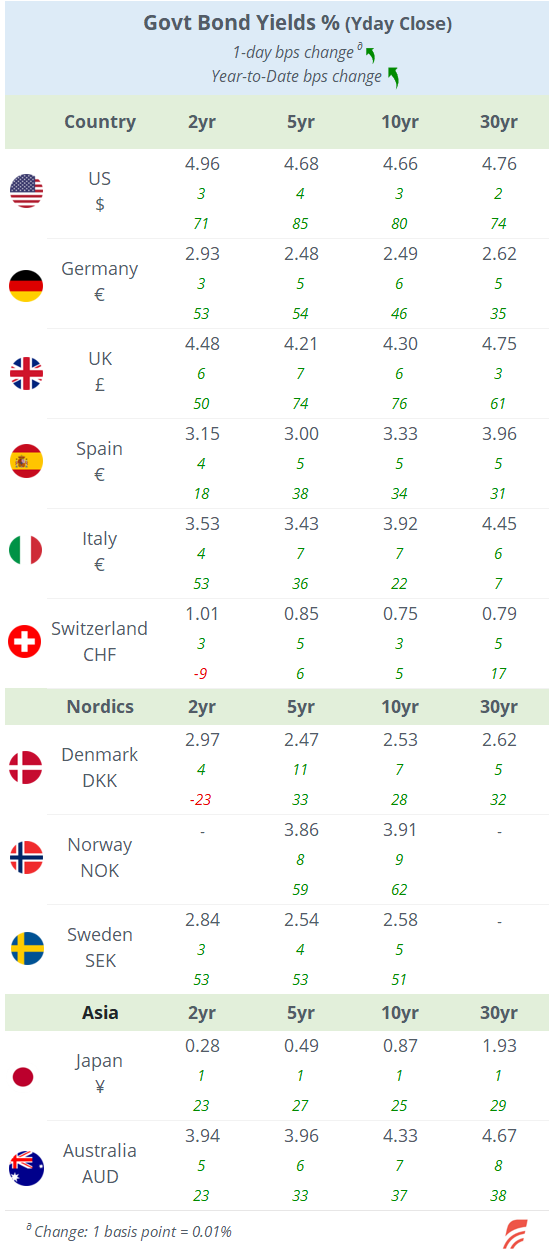

Currency markets were little changed yesterday but the dollar continues to appreciate, accumulating a 2% weekly gain against majors and more than 3% against the Aussie and Kiwi dollars. Benchmark yields edged a few basis points higher across all markets and tenors.

Crude oil is remarkably calm with Brent below $90 this morning. Asian stocks are mostly firmer and European futures are anticipating a higher opening.

In economic data updates, UK unemployment rose to 4.2%, exceeding estimates and average earnings grew by 5.6% YoY, unchanged from a month earlier. Italian inflation in March was revised lower to 1.2%, while CPI in Canada printed at 2.9% and Core inflation at 2.0%. Data in the US came in mixed with a weaker property market as building permits (1.458mn) and housing starts (1.321mn) were below expectations, but industrial (0.4% MoM) and manufacturing (0.5% MoM) output were in line with estimates.

Corporate deals worth mentioning: Europe’s largest asset manager Amundi, announced a partnership with US asset manager Victory Capital that includes a 26% stake for Amundi without a cash investment. Victory’s shares added 3.5% to a total market value of $2.75bn, equivalent to a fifth of Amundi’s market cap.

International Paper of the US confirmed it is taking over British packaging company DS Smith for £5.8bn in an all-share deal. DS Smith shareholders will own nearly 34% of the merged company. Shares fell 4% yesterday.

On the IPO front, Microsoft-backed cybersecurity software company, Rubrik, is planning to raise $713mn at a $5.45bn valuation in the NYSE, with a price guidance range of between 28 and $31. It will trade under the symbol RBRK.

Digital marketing firm Ibotta, backed by Walmart, is also in line for a public offering to raise $472mn, targeting a $2.5bn valuation with a price guidance range of 76 to $84. It will also be listed on the NYSE and use the symbol IBTA.

In credit markets, German government-owned transport company, Deutsche Bahn Finance, raised €500mn with a 10-year senior bond, rated AA-, at 90 bp over Bunds or a 3.40% yield.

In economics today, we’ll get inflation updates in the €-zone and the UK and mortgage data in the US.

That’s all for today, see you tomorrow.