Markets Dawn Europe: Wed 15 by 7AM UKT (8AM CET)

Brief Podcast 🎙 + Data 📊 + Script 📄

Script: Estimated reading time ⏲ ~5 mins

Good morning,

Let’s begin with today’s headlines. Putin will visit Xi Jinping in China in a sign of the two countries' close ties while Washington threatens Beijing with sanctions over its support for Russia.

The US has sharply increased import tariffs on Chinese electric vehicles and chips, impacting $18bn worth of goods coming from China. Although only 2% of US imported electric cars come from China, the import tax will quadruple. The cost of importing Chinese batteries, aluminium, steel, solar panel cells and semiconductors will also rise sharply.

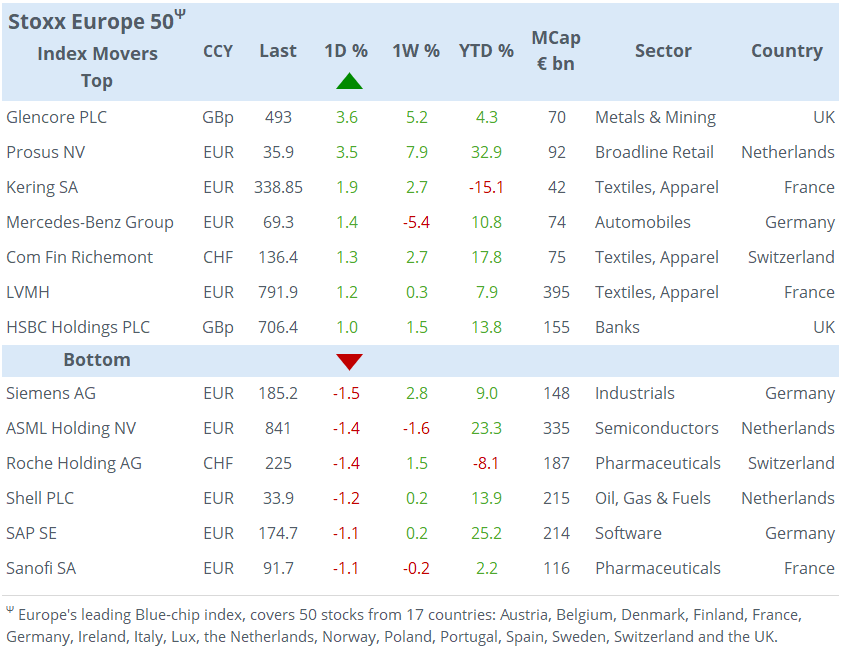

Onto markets, risk assets maintain a firm tone with stocks adding more than 0.5% in the US and the Stoxx 600 closing modestly higher to a record, with an outperformance by Spanish, Italian and Austrian names. The IT sector helped the Nasdaq index reach an all-time high.

In forex, the $ continues to slowly depreciate against the € and £ but remains firm against a weakening ¥. Bond markets were mixed and little changed, the Bunds curve shifted a few basis points higher, Gilts were flat and Treasury yields fell 4bp across tenors.

Fed Governor Powell made dovish remarks yesterday in the Netherlands, signalling that the Fed is not planning to hike rates and that the current policy rate is, by many measures, already restrictive. He highlighted the strength of the US economy and thinks that inflation will drop but he’s not as confident as in the recent past. Today’s retail inflation update will be key for markets.

Asian markets are mixed today, Japan is flat, Singapore is softer and Taiwan is gaining 1%, while Hong Kong and Korea are shut for holidays. In Tokyo, Sony Group shares are rallying 9%, their best day in three years, after announcing solid results and a $1.6bn share buyback. Sony shares are nearly unchanged YTD to a market cap of $104bn.

European futures this morning are signalling a positive market open with the FTSE up almost 0.4%. Brent oil is higher at $82.90 and Bitcoin is little changed at $61,900.

In economics, the main data release yesterday was US PPI or producer prices which rose by 0.5 MoM, above estimates, and 2.2% YoY, higher than the 1.8% a month earlier. Also, EU-harmonized inflation in Germany was confirmed at 2.4% YoY and in Spain at 3.4%. Unemployment in the UK rose marginally to 4.3% as employment change fell by 177k, although not as bad as anticipated.

The miners' saga continues as Anglo American announced plans to refocus on copper while divesting from its less profitable nickel, coal and precious metals units, as it tries to convince shareholders it can achieve greater value without BHP. Anglo is even exploring an IPO for its De Beers diamond business. Shares dropped more than 3% yesterday.

The new issue market remains active for euro-denominated bonds, with several corporates placing multiple tranches. These include Johnson & Johnson (8, 12, 20yr), Air France (5yr), Illinois Tool Works (8yr), Novo Nordisk (5, 7, 10yr), Ferrari (6yr), Lottomatica (6yr), among others.

In credit ratings, the British online supermarket company, Ocado Group, was downgraded two notches by Fitch to B- (outlook stable), deeper into junk territory.

Today brings the highly awaited headline and core CPI inflation in the US at 13:30 London time. Analysts expect the headline monthly reading to increase by 0.4% and the annual figure to moderate to 3.4%. We’ll also get US retail sales, inflation in Sweden, and GDP and industrial production in the €-zone.

Companies reporting today include Allianz, EON, RWE, Commerzbank, and most Japanese banks.

That’s all for today, see you tomorrow.

Copyright © 2024 Laconic. All rights reserved. This publication, 'Markets Dawn Europe,' contains proprietary content and is intended solely for the recipient's personal use. Please share using the button below, as access is free to all.