Markets Dawn Europe: Wed 10 by 7AM UKT (8AM CET)

Brief Podcast + Data + Script

Podcast ↑↑↑↑ Scroll down for the script

Good morning,

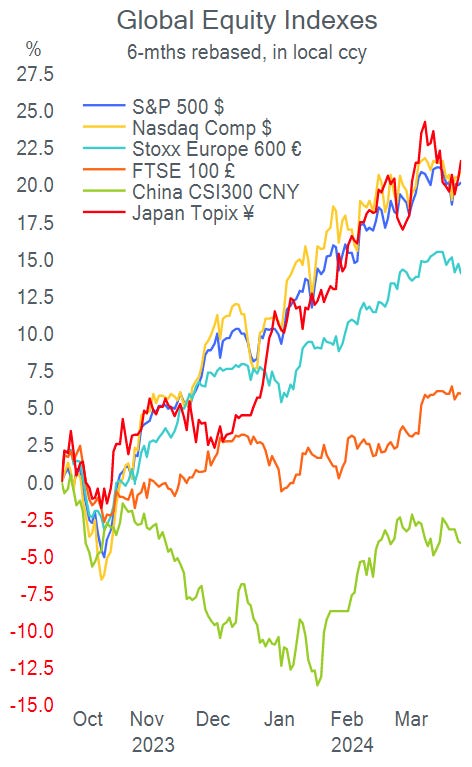

Wall Street posted modest gains yesterday ahead of today’s inflation update and the earnings season that begins on Friday with major banks. Traders’ focus remains on the timing of the first Fed rate cut and today’s update will be a key data point. There are no significant single stock movers in the US to highlight.

European stocks fell across markets yesterday, the Eurostoxx 50 lost 1.1% with German and Italian indices as the weakest on the back of a sell-off in the defence sector. The main losers were Saab, Leonardo, Rheinmetall, Thales and BAE, all down between 5 and 10%. Equity index futures are pointing to a better open this morning, up more than 0.5%.

Benchmark yields reversed around 7 basis points yesterday across markets, with 10-year Treasuries closing at 4.37%. Bonds ended at 2.37% and Gilts at 4.03%. Forex markets were little changed, both the euro and sterling appreciated 0.8% against the dollar in the past seven days.

Headlines,

Fitch downgraded China’s debt outlook to negative this morning, and forecast the public deficit to widen to 7.1% of GDP this year. The credit rating was affirmed at A+. Fitch forecasts Chinese economic growth to moderate to 4.5% in 2024 from 5.2% last year. Stocks in mainland markets are down 0.5% while the Hang Seng is gaining nearly 2%. The yuan is steady at 7.23.

South Korea holds legislative elections today. The two main parties are the ruling People Power Party and the main opposition Democratic Party of Korea. Markets are closed today. The Kospi index fell 0.5% yesterday.

The Italian government cut its growth estimate for this year to 1% and 1.2% for next year and anticipated higher public debt on the back of a weaker growth outlook. Rome estimates a debt-to-GDP ratio of 138% for 2024. 10-year BTP yields fell 8 bp yesterday to 3.72%.

Tuesday was a quiet day in corporate deals. L’Occitane International, the Luxembourg-based and Hong Kong-listed beauty products company may be taken over by its largest shareholder, with debt financing provided by Blackstone. L’Occitane’s market cap stands at $5.55bn and shares were suspended yesterday ahead of an announcement.

HSBC continues to reduce its international footprint by selling its Argentina subsidiary for $550mn to a local banking group. HSBC will book a $1bn loss on the exit.

There were a few corporate bond issues in the Euro market worth highlighting. Porsche placed two senior tranches of benchmark sizes, a 5.5-yr at swaps +115 bps and an 8.5-yr at +150. Japanese brewery Asahi also placed 5 and 8-yr senior bonds, rated Baa1, at 65 and 150 bp over swaps. Finally, Britain’s BAT placed 8-yr bonds rated BBB+ at +150 bp.

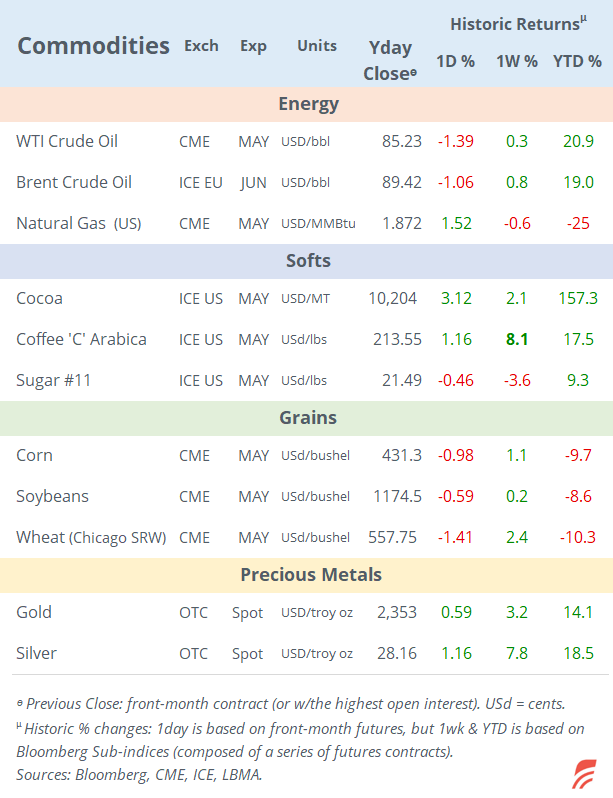

In today’s economic front, the main release will be US headline and core CPI inflation for March, with consensus expecting a small increase to 3.4% YoY for headline CPI. European countries updating on inflation include Portugal, Norway and Denmark.

In monetary policy, the Reserve Bank of New Zealand kept its cash rate unchanged as expected at 5.5% this morning. The Bank of Canada will meet later today, with analysts anticipating the 5% policy rate to remain unchanged. However, futures markets are pricing in a 24% probability of a 25 bp cut.