Markets Dawn Europe: Tue 7 by 7AM UKT (8AM CET)

Brief Podcast 🎙 + Data 📊 + Script 📄

Script: Estimated reading time ⏲ ~4 mins

Good morning,

Stocks on Wall Street had another strong day with the S&P 500 and Nasdaq adding another percentage point, maintaining Friday’s positive momentum. Market sentiment improved on renewed expectations of a more dovish Fed. European benchmarks also traded firmer with the Eurostoxx 50 closing 0.7% higher and Italian and German equities as the outperformers.

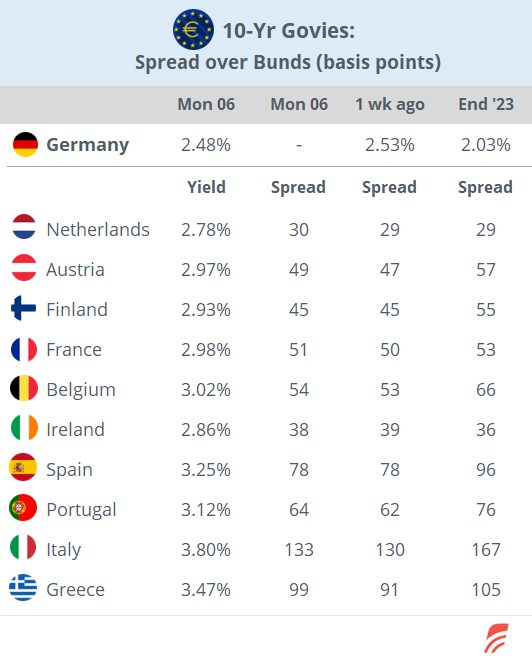

Sovereign bond markets barely changed yesterday with the Bunds yield curve shifting marginally lower while Gilts ended almost unchanged on low liquidity. 10-year Bunds closed at 2.48% and Gilts at 4.25%. A similar story over in the US with Treasuries closing at 4.49%.

With London out on bank holiday, currencies had a quiet day with the yen declining modestly after its sharp reversal, but it is accentuating its decline today.

Headlines,

-Israel carried out air strikes on Rafah, Gaza’s southern city where 1mn people are living after they escaped from the conflict area. The incident took place after Israel warned residents of the attack and soon after Hamas proposed terms for a ceasefire. Netanyahu said that Hamas's proposal was far from his basic requirements and that negotiations continue.

-The US FAA opened a new Boeing inquiry to investigate proper inspections of all 787 Dreamliner aircraft still in production. Shares ended marginally weaker.

-Australia’s central bank kept its policy rate steady today at 4.35% as inflation remains high and is falling slower than the RBA anticipated.

In economics, producer prices in the €-zone fell more than expected, down 7.8% YoY in March and February was revised lower to -8.5%, maintaining the downward trend of wholesale prices. The Sentix index, an indicator of investor morale in the €-block improved for a 7th straight month to its highest level in 2 years. The €-zone’s Services PMI survey also printed above estimates showing an expansion in activity mainly in Spain, Italy and France.

In corporate deals, US clean energy operator Alette is being acquired by Canada’s CPPI and Global Infrastructure Partners in a deal worth $6.2bn including debt.

In the Spanish banking sector, Banco Sabadell’s board rejected BBVA’s €12bn takeover approach late yesterday, on the basis that it significantly undervalues the bank’s standalone growth potential. Sabadell shares closed at an all-time high for a total market cap of €10bn.

Softbank, Nvidia and Microsoft are investing $1bn in British self-driving car start-up Wayve, the largest investment for a European artificial intelligence company.

In debt capital markets, the notable issuer yesterday was Coca-Cola with three benchmark-size senior dollar bonds (rated A1) with 10, 30 and 40-year maturities. The 2054 was priced at T+70bp and the 2064 at +80bp.

On today's data, we’ll get retail sales in the €-zone, construction PMIs in €-zone countries, UK house prices, Dutch inflation, Germany’s trade figures, industrial orders and manufacturing output. On the earnings front, Ferrari, Infineon, Deutsche Post, Bouygues, Disney and Occidental Petroleum report today.

European equity futures are trading firmer this morning and Asian markets, except for China, are also 0.5 to 1% higher.

That’s all for today, see you tomorrow.

Copyright © 2024 Laconic. All rights reserved. This publication, 'Markets Dawn Europe,' contains proprietary content and is intended solely for the recipient's personal use. It is prohibited to copy and paste, forward, or set up auto email forwarding rules to give access to others. Please share the publication using the button below, as access is free to all.