Markets Dawn Europe: Tue 6 Aug

Podcast 🎧 Extended Transcript 📄 Data 📊 Charts 📈

Markets are bouncing back from yesterday’s steep sell-off with Tokyo rallying 7% and Taiwan and Korea gaining around 3%. European and US stock futures are up by more than 1% and bond futures are falling sharply overnight.

Monday’s global equity risk-off sentiment was triggered by fears of a US recession following weak data at the end of last week which led to the wipeout of more than $6tn of global market value. Fed officials tried to reassure markets that the US is not in a recession and reaffirmed the central bank goals of price stability, maximising employment and maintaining financial stability. The probability of a 50bp rate cut in September rose to 72%.

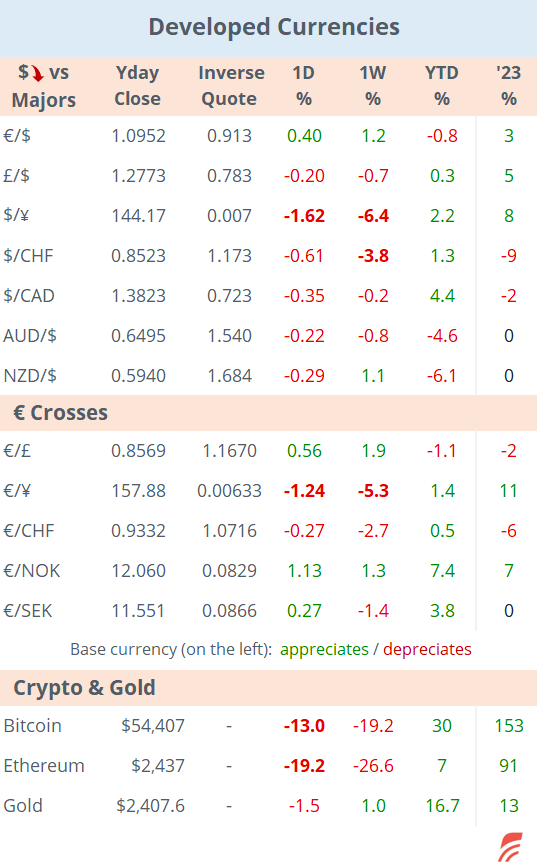

Bond markets ended little changed so we’ll focus on the action. The unwind of popular trades hit Japan the hardest with stocks posting their second-worst day in history and worst since October 1987 with a 12% decline. Some Japanese blue chips lost a quarter of their value in just five sessions, including Toyota, MUFG, Softbank Group and Mizuho. The ¥ appreciated again and accumulated a 6.4% rally in the last seven days while bond prices jumped yesterday with 5-yr JGB yields dropping 21bp to 0.37%.

To put the Japanese market move into perspective, the broad Topix stock index had rallied 24% to its all-time high three weeks ago. As of yesterday’s close, it had lost 24% from that record and was 6% lower YTD. Measured in $ and before today’s recovery, the index was down 8% YTD.

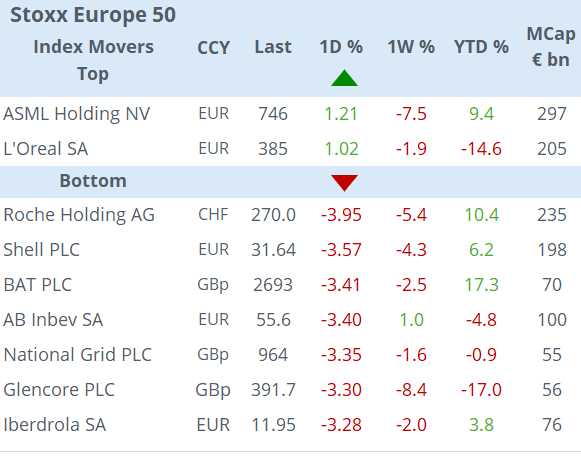

In the US and Europe, the sell-off was broad-based with every sector declining by almost the same amount and no single stock was the centre of weakness. The S&P 500 and Nasdaq 100 lost 3% and the Stoxx 600 fell 2.2%. Indices reduced their YTD gains significantly and the Nasdaq is now 6% higher this year, the Stoxx 600 is up by just 2% and the French CAC 40 is down 5%. In volatility markets, the VIX index traded as high as 66%, the highest in four years, before closing at 38.6%,

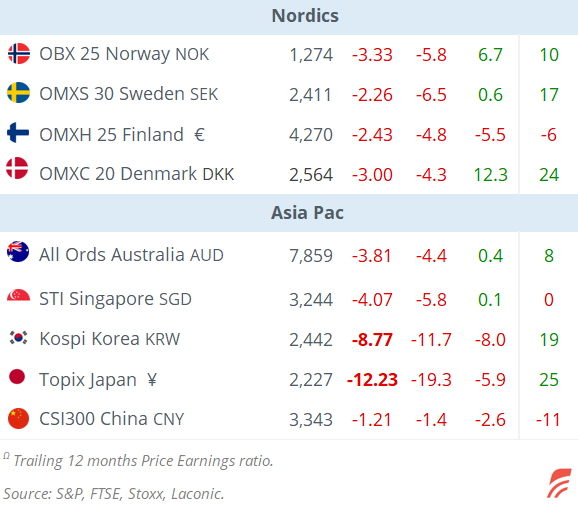

Unsurprisingly for a severe risk-off day, emerging market stocks followed their developed peers but except for Taiwan losing more than 8%, all other markets fell in line with Wall Street (see table). Cryptos were big losers on Monday with Ethereum down 19% and Bitcoin retreating 13% to its lowest level in five months.

Today, the Reserve Bank of Australia left its policy rate steady at 4.35% as expected, mainly because inflation remains above target and is proving persistent. Short-end Aussie yields rallied in recent sessions and are now trading around 3.7%.

Headlines:

-Iran threatens to ‘punish’ Israel for the killing of Hamas’ leader in Tehran.

-Google lost an antitrust case over its online search dominance. Alphabet shares fell 4.4% yday and are +14% YTD.

In corporate deals, SocGen is selling its British and Swiss private banking divisions to UBP of Switzerland for €900mn.

US snack giant Mars (unlisted) is exploring the acquisition of Pringles maker Kellanova (mcap $25bn). Kellanova shares climbed 16%.

In private markets, Carlyle is selling US independent power producer Cogentrix Energy for $3bn to another private equity firm, Quantum Capital.

Data today: €-zone retail sales; German industrial orders; Dutch inflation; US international trade; Canadian trade balance.

Earnings: Caterpillar, Uber, Airbnb, Bayer.

Copyright © 2024 Laconic. All rights reserved. This publication, 'Markets Dawn Europe', contains proprietary content and is intended solely for the recipient's personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.