Markets Dawn Europe: Tue 28 May

Podcast 🎙 Data 📊 Script 📄

Podcast script: Estimated reading time ⏲ ~4 mins

Good morning,

Asian markets are trading mixed today with China and Australia moderately weaker while Hong Kong, Taiwan and Singapore are notably firmer and Japan is flat following a robust day for €-zone stock markets on a holiday for the UK and US.

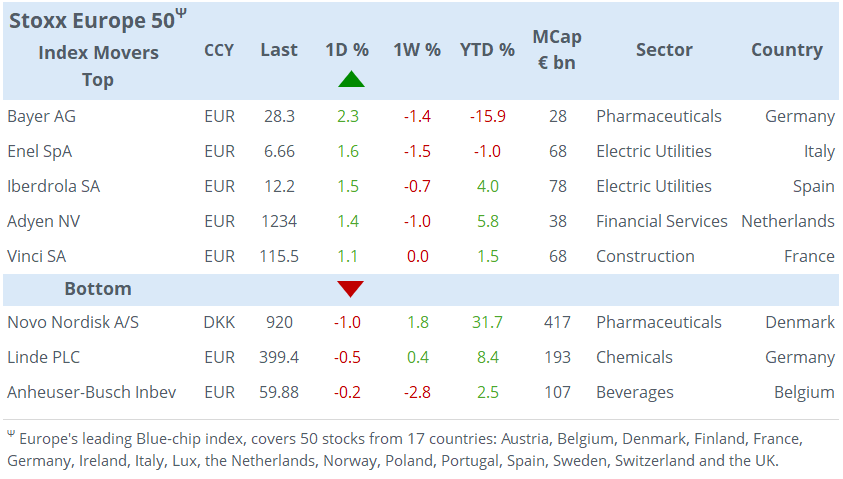

The €-Stoxx 50 gained nearly 0.5% yesterday with the Spanish (+0.7%) and Italian (+0.8%) benchmarks as the outperformers with the utilities and oil and gas sectors as the biggest gainers.

The catalyst for the positive sentiment at the start of the week was encouraging comments by ECB officials regarding an almost certain 25bp policy rate cut to 3.75% at next week’s meeting. ECB’s chief economist, Philip Lane, said that subject to this week’s key inflation data updates, the central bank is ready to lower the restrictive level of rates but that the rest of the year will be bumpy and gradual, and markets should not expect the beginning of a series of cuts. His comments were in line with remarks by the head of the French Central Bank Villeroy who suggested the ECB should be free to pause following a cut in June.

The Swedish and Swiss central banks have already reduced borrowing costs this year while the Fed has indicated it will wait until the disinflation trend is confirmed.

There were no significant stock movers among Europe’s large caps with Bayer as the biggest winner among Stoxx 50 members with a 2.3% gain. French train manufacturer Alstom launched a €1bn rights issue to improve its finances and saw shares advance 5.5% to a 7-month high and a total market cap of €7.6bn.

It was a quiet day for data releases but the German Ifo indicators reflected that business sentiment stagnated in May. The country’s most prominent leading indicators, including business climate (89.3), current economic conditions (88.3) and expectations (90.4) came in below analysts’ estimates.

Headlines,

-Israel’s latest airstrikes on the city of Rafah killed 45 at a tent camp triggering an outcry from global leaders as Netanyahu’s decision backfired. Israel’s military said that the attack was based on precise intelligence and that the Hamas chief of staff was killed. But the collateral damage of this operation was condemned by French President Macron among others, as they urged Friday’s UN court ruling to be implemented.

-Elon Musk’s artificial intelligence project xAI, raised $6bn from VC firms, Andreessen Horowitz and Sequoia Capital, for a post-investment valuation of $24bn to become a clear competitor to OpenAI and Meta’s initiative.

-US stock market trades will begin to settle on a T+1 basis from today.

In data today we’ll get Germany’s wholesale prices, Ireland’s retail sales, US consumer confidence and Canada’s producer prices.

In credit rating updates, Fitch upgraded by one notch the following Australian banks: Westpac (AA-), Macquarie (A+), ANZ (AA-), NAB (AA-) and CBA (AA-). Moody’s upgraded Italian bank BPER Banca to Baa3.

That’s all for today, see you tomorrow.

Copyright © 2024 Laconic. All rights reserved. This publication, 'Markets Dawn Europe,' contains proprietary content and is intended solely for the recipient's personal use. Please share using the button below, as access is free to all.