Markets Dawn Europe: Tue 23 by 7AM UKT (8AM CET)

Brief Podcast 🎙 + Data + Script

Podcast 🎙 ↑↑↑↑ Scroll down for the script.

Podcast script: Estimated reading time ⏲ ~5 mins

Global stocks ended higher yesterday with US indices posting a partial reversal following six straight days of falls. The S&P 500 and Nasdaq closed ~1% higher last night after Europe’s firmer close with the FTSE 100 advancing 1.6% to 8,024 points, an all-time high. This week's focus is on earnings reports on both sides of the Atlantic.

Britain’s blue-chip index is dominated by international companies whose earnings benefit when sterling depreciates. The 3% YTD fall for the pound and the prospects of a Bank of England rate cut, helped the FTSE 100 gain 4% this year. It still lags the 9% gain by the €Stoxx 50.

Portugal’s PSI 20 index outperformed yesterday with a 3.5% rally on the back of Galp Energia’s 20% jump to its all-time high. Galp announced plans to sell half of its 80% stake in a Namibia offshore oil field which is said to contain more than 10bn barrels of oil. Galp is now worth €15bn.

Some notable stock movers in the US yesterday include Ford, adding 6%, Nvidia more than 4% and Bitcoin-related names, Coinbase up by 7% and Microstrategy rallying 13%.

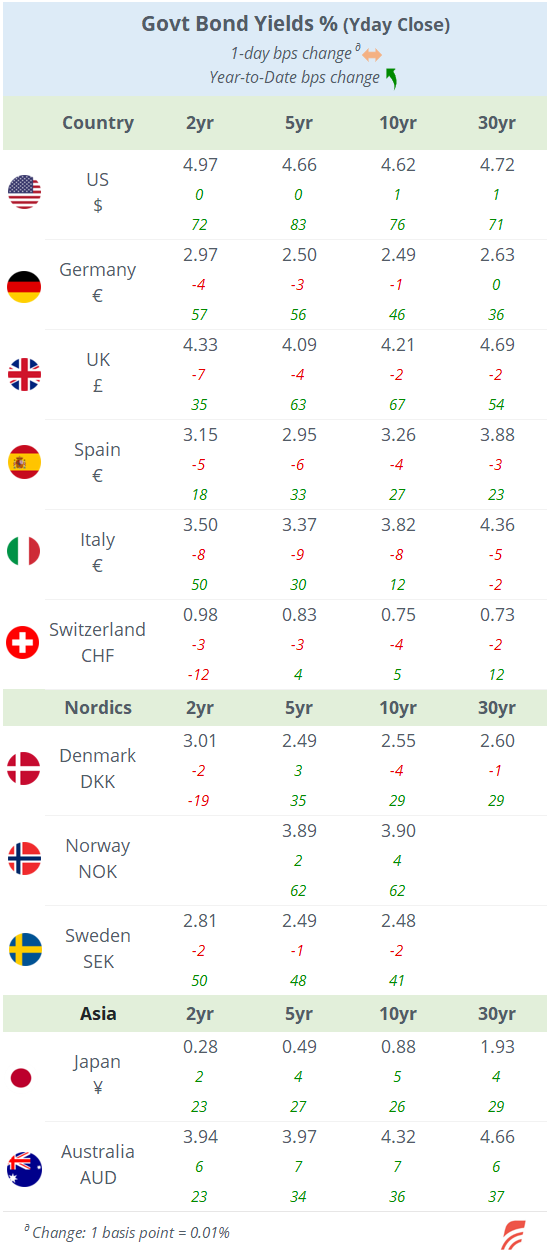

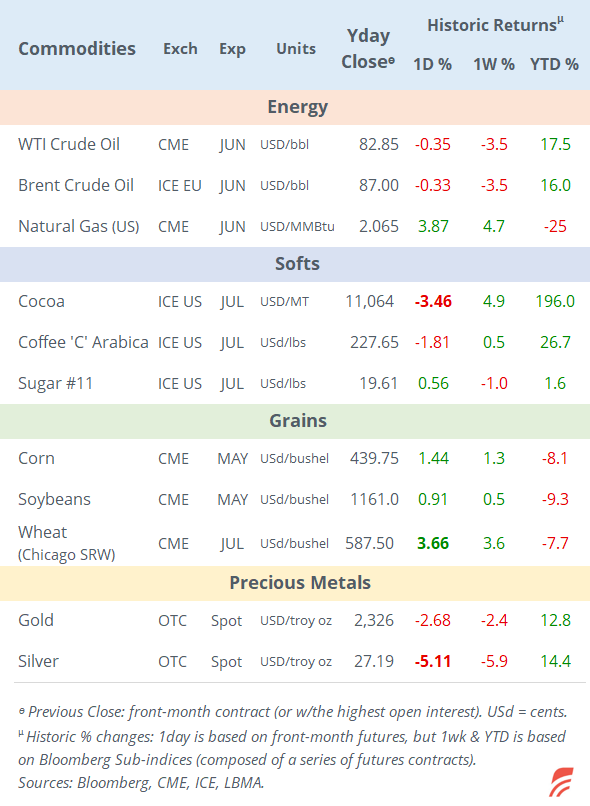

Currencies and benchmark yields were little changed yesterday. The yen fell marginally but reached another multidecade low against the dollar of shy of 155 as interest rate outlooks between the Fed and the Bank of Japan diverge. Gold had its worst single-day fall in over a year, down nearly 3% to $2,326 while Silver plunged more than 5%, mainly due to lower demand for safe-haven assets as Middle East tensions ease.

Asian markets are maintaining a positive tone today, with Hong Kong, Singapore and Taiwan benchmarks up by more than 1% while mainland China is 0.5% softer. European stock futures are also firmer this morning.

Headlines,

- The so-called ‘hush money case’ against Trump began yesterday, with the presidential candidate accused of attempting to corrupt the 2016 election by buying the silence of a woman.

-London joins Washington in sending more long-range missiles to Ukraine in its largest aid package.

On earnings reports, German software giant SAP released figures last night after the European market close. It met revenue (€8bn, +8.1% YoY) estimates but missed net profit expectations (-€828mn) with a loss due to the provision to cover expenses of its €2.2bn restructuring plan. Shares in New York ended marginally higher driven by the 24% improvement in sales of its cloud computing unit. SAP’s market value stands at €204bn and is 19% higher YTD.

In corporate deals, US-online property marketplace CoStar Group will acquire Matterport, a software company that builds 3D virtual tours, for $1.6bn in a stock-and-cash deal. Matterport’s shares rallied 175% yesterday.

IPOs remain active, with cruise operator Viking Holdings (VIK) launching its public offering yesterday with a valuation target of nearly $11bn and setting a price range of $21 to 25. Viking is backed by TPG and the Canadian pension fund CPP.

British private equity firm CVC Capital Partners’ IPO will be priced towards the end of the week in the Dutch exchange, with a target market value of €15bn and an indicative price range of €13 to 15. It will sell around 11.5% of the company.

In debt capital markets, Procter & Gamble is issuing two senior bonds rated AA- (4 and 10-yr) for a total of €1.5bn to be priced today.

In data today, we’ll get manufacturing and services PMIs for the US, €-zone, UK, Germany and France.

Companies reporting earnings today include Tesla, Novartis, GE, Visa, Lockheed, UPS and Pepsico among others.

That’s all for today, see you tomorrow.