Markets Dawn Europe: Thu 20 Jun

Podcast 🎙 Data 📊 Script 📄

Morning,

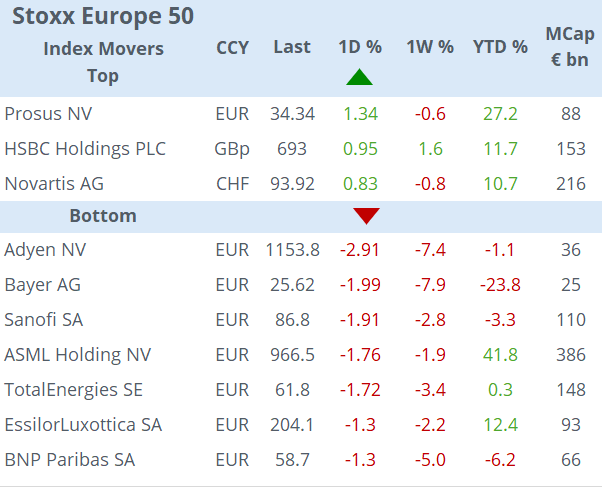

European equity markets ended a touch softer on average with French stocks underperforming with a 0.8% drop on a calm trading day due to the US holiday. The weakest sectors were real estate and technology without significant moves among large caps. Interest rate and currency markets were little changed with the $ ending marginally weaker and benchmark yields just 1-2bp higher.

The main data update was UK inflation which showed a deceleration for headline CPI to 2%, the first time it hit the central bank’s target since 2021. The reading was better than expected and below April’s 2.3%. However, services price inflation, a measure closely watched by the Bank of England, was 5.7% exceeding the forecast but lower than a month earlier. We’ll learn what Governor Bailey thinks of this mixed update at today’s press conference. Markets are not anticipating a rate cut at today’s meeting, ahead of the general election.

China’s central bank maintained its Loan Prime Rates unchanged as expected. The one-year, used for corporate loans, at 3.45% and the 5-yr, used as a reference for mortgages, at 3.95%. The latest property market data shows that prices for new homes dropped at the fastest rate in a decade. Real estate stocks are pulling mainland and Hong Kong indices lower today by 0.5%. Other Asian markets are also trading in red today with Japan leading the fall while Korea and Taiwan are the only equity markets making marginal gains.

European stock futures are pointing to a better open in early trading, up 0.2% on average while Bund futures are a touch lower. Nasdaq futures are nearly 0.5% firmer in overnight trading. Currencies in Asia are little changed with the yen trading above 158. Brent oil is steady at $85 and Bitcoin is around $65,000 this morning.

Headlines,

-Putin visits Vietnam following a trip to North Korea where he agreed to a mutual military aid in the event of a foreign attack.

-The ECB has warned €-zone nations to reduce their debt burdens by an average of 5% of GDP. Rising spending on defence, climate change and demographics have added significant fiscal pressure.

-Brazil left its monetary policy rate steady at 10.5% in a unanimous decision by Copom, following several rate cuts in the past meetings, on the back of higher inflation expectations and forecast for a delay in the Fed easing its policy. President Lula da Silva renewed his criticism against the central bank saying that monetary policy was the only thing out of place in the country. Inflation in Brazil is running slightly below 4%, within target and the currency has depreciated 11% YTD to 5.42.

Today will be an active day for central banks, with the Swiss National Bank announcing at 8:30 London time, Norges Bank at 9:00 and the Bank of England at noon. The SNB is expected to cut rates by 25bp for a second consecutive meeting to 1.25%. The Swiss franc has been the strongest currency among majors in the past 7 days with gains of 1.7% against the €. Norges and the BoE are expected to keep interest rates unchanged at 4.5% and 5.25%. Indonesia’s central bank also meets today with analysts anticipating no rate change at 6.25%.

In data updates, we’ll get Germany’s producer prices and US housing figures. On the earnings front, Accenture (mcap $191bn) will report today.

See you tomorrow.

Copyright © 2024 Laconic. All rights reserved. This publication, 'Markets Dawn Europe,' contains proprietary content and is intended solely for the recipient's personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.