Markets Dawn Europe: Mon 23 Sep

Podcast 🎧 + Transcript 📄 + Tables 📊 + Charts 📈

Hi, Markets Dawn Europe is ads-free. To survive, it needs to grow its audience, get more feedback and support. 🙏 share it, like it and email us with suggestions so we can improve.

Morning,

European stocks finished on a weak note on Friday on the back of poor performance for the Auto sector and a steep drop for Novo Nordisk (-5%) following a disappointing revenue update for its obesity drug. Europe’s largest co was last week’s worst-performing blue chip with a 7.5% decline. Indices fell up to 1.5% across Europe on Friday and the Stoxx 600 ended the week with a modest drop. Wall Street had a positive week with the S&P 500 reaching another record on Thursday following the Fed’s rate cut and the index is now 20% higher YTD, outperforming all other global benchmarks in local currency. The soft landing scenario for the US economy is gaining momentum.

In earnings reports, the notable announcement on Friday was Fedex’s (mcap $62bn) disappointing quarterly profit drop and a lower annual revenue forecast due to weak economic conditions. Shares plunged 15%, their worst day in 2-yrs., dragging the logistics sector lower.

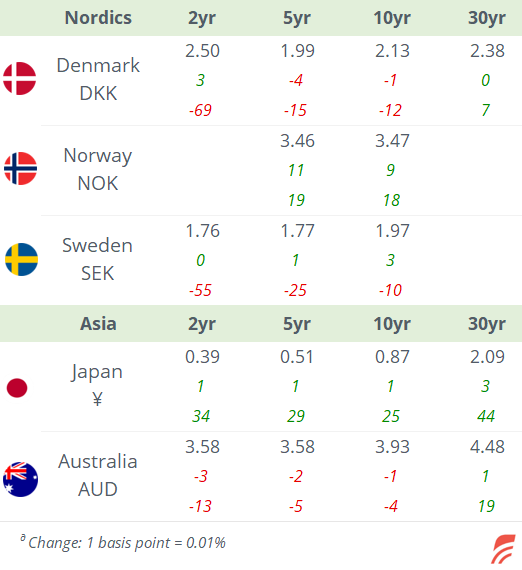

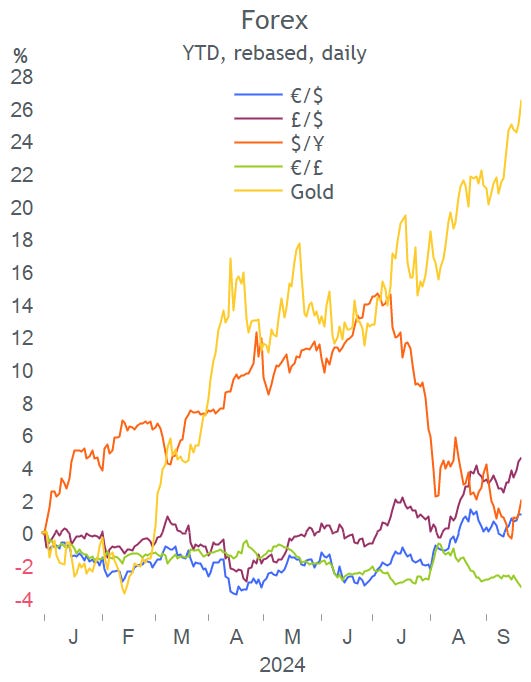

In forex markets, the $ index ended the week unchanged but the greenback depreciated against £ and the € but appreciated vs the ¥. Gold advanced nearly 2% to a fresh record while cryptos added 5%. Benchmark interest rates shifted higher last week with 10-yr Treasury yields adding 8bp to 3.73%, Bunds up 7bp to 2.22% and Gilts jumping 13bp to 3.9%.

It was a busy week for central banks. Besides the Fed’s jumbo rate cut, we heard from the Bank of England (unch at 5% as exp), Norges Bank of Norway (unch at 4.5% as exp), the Bank of Japan (unch at 0.25% as exp, signalled rates to remain steady), South Africa (-25bp tp 8%), Turkey (unch at 50%).

Also, China left lending rates (LPR) unch at 3.35% for 1-yr and 3.85% for 5-yr on Friday but today the PBoC cut its 14-day reverse repo rate to 1.85% to ease monetary conditions.

Asian markets are trading mostly firmer today with indices gaining up to 0.70% except for Australia which is a touch weaker. The main driver was China’s central bank rate cut. Japanese markets are closed for a holiday. Brent is shifting upwards and is now above $75. European and US equity futures are pointing to a higher open in overnight trading.

In credit ratings, Croatia was u/g one notch by Fitch to A-, Iceland was u/g one notch by Moody’s to A1 and Portugal’s outlook was u/g to positive by Fitch.

On the data front, an active week begins with preliminary PMIs for September in developed countries today and will include US GDP and PCE inflation later in the week. In monetary policy announcements, we’ll hear from central banks in Australia (tomorrow, expected unch at 4.35%), Sweden, Switzerland and Mexico. It will be a light week for corporate earnings releases.

Copyright © 2024 Laconic. All rights reserved. This publication, 'Markets Dawn Europe', contains proprietary content and is intended solely for the recipient's personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.