Markets Dawn Europe: Fri 5 by 7AM UKT (8AM CET)

Brief Podcast + Data

Podcast ↑↑↑↑ Scroll down for the script.

Good Friday,

US stocks sold off sharply towards the end of the trading session last night, as investors await today’s key employment data and digest new comments by Fed policymakers.

Every leading US benchmark fell around 1.3% with all sectors falling. The VIX volatility index had its biggest daily jump since October to 16.3%, its highest level in 4 months.

Among the hawkish comments yesterday, Minneapolis Fed President Kashkari said that if inflation continues to stall, no rate cuts may be required this year. Richmond Fed President Barkin said that the Fed has "time for the clouds to clear" on inflation before starting to cut rates. These remarks follow Powell’s cautious comments on Wednesday.

European equity indices barely changed yesterday but futures are trading weaker this morning, down 1.5%. All Asian stock markets are lower today, with Tokyo and Korea down 1%.

Headlines,

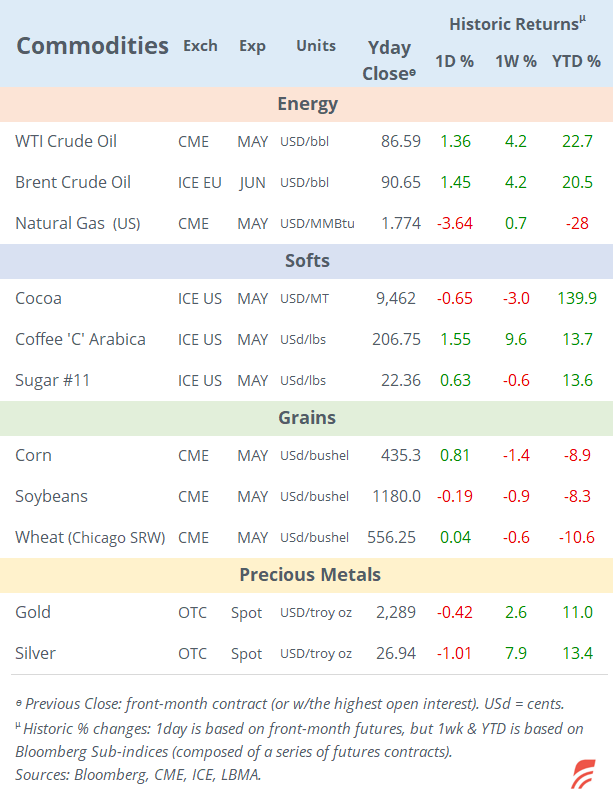

Washington called for an immediate ceasefire in Gaza following Israel’s mistake in the killing of aid workers. Biden urged Netanyahu to protect civilians or risk losing the support of the US. The geopolitical tensions pushed Brent prices above 90 for the first time in 5 months.

Today, India’s central bank kept its policy rate unchanged for the seventh consecutive meeting, as expected, at 6.5%. The RBI sees solid economic growth and expects inflation to drop.

US Treasury Secretary Janet Yellen is in China as Washington and Beijing try to improve bilateral relations. On the agenda is trying to avoid large exports of cheap green technology that China has accumulated, to protect the US solar and battery industries.

French luxury group Kering acquired a prime retail property in Milan for €1.3bn from Blackstone, Europe’s largest real estate deal in 2 years. The location already houses a Saint Laurent boutique as well as competing brands.

In economic updates, Swiss inflation eased further during March, to the lowest in two-and-a-half years, 1% YoY and unchanged for the month. The Swiss National Bank was the first leading central bank to cut rates this year to 1.5%, and this reading supports more policy easing.

In Europe, the services sector continues to expand contrasting with a weakening manufacturing sector, as composite PMIs for most countries reflect a return to growth for the first time in almost a year. The strongest services PMIs were in Spain, Italy and the UK. Producer prices in the Eurozone fell more than anticipated, down 1% in February and 8.3% in the last 12 months.

The US trade deficit widened in February to $69bn on strong imports, despite exports reaching an all-time high of $263bn.

Poland’s central bank kept rates unchanged at 5.75%, as expected, despite inflation fall.

In company deals, media reports suggest that Google’s parent Alphabet is considering a bid for US digital marketing software company HubSpot, which has a market value of $32bn. HubSpot shares gained 5% yesterday.

Wendel, the French investment company plans to sell a 9% stake in Bureau Veritas, the French business support company, for around €1.1bn via an accelerated bookbuild. Wendel is Veritas' largest shareholder.

In debt capital markets, French auto parts, Valeo, raised €850mn with a 6-year senior green bond priced at a 4.61% yield.

Also, Spanish oil and gas CEPSA Finance, raised €750mn with a 7-year senior bond at 188 bps over Bunds, or a 4.20% yield. Both issues are rated investment grade.

Today, we’ll get US non-farm payrolls plus all the related employment data for March and retail sales in the Eurozone.

That’s all for today, have a nice weekend.