Markets Dawn Europe: Fri 24 by 7AM UKT (8AM CET)

Podcast 🎙 Data 📊 Script 📄

Podcast script: Estimated reading time ⏲ ~5 mins

Good morning,

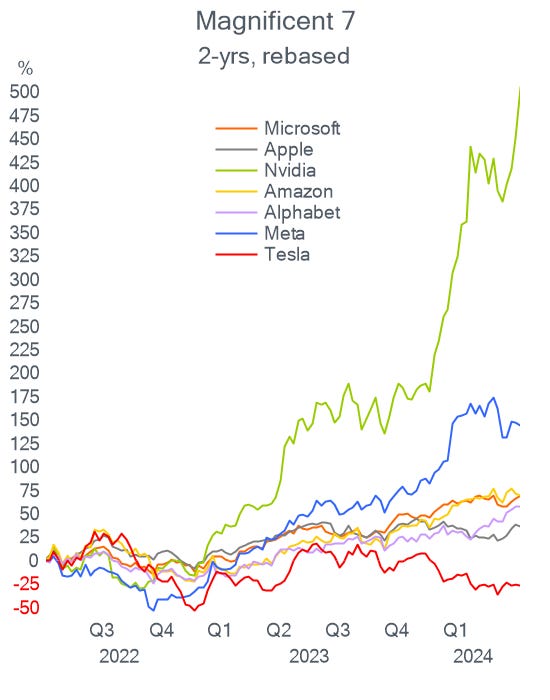

Nvidia’s record profits and 10% stock rally were not enough to stop Wall Street from selling off sharply during the afternoon. Benchmark indices were trading firmer overnight following Nvidia’s earnings release (on Wed) but the Nasdaq 100 reversed and dropped by 2% intraday to end the day lower by less than 0.5%. Three days after breaking the 40,000-point mark, the Dow Jones Industrials posted its worst day this year with a 1.53% decline with every member falling and Boeing as the biggest loser, down 7.5%.

The catalyst was robust PMI data that suggests that inflation remains a concern, potentially delaying a Fed rate cut and investors still digesting the mostly hawkish meeting minutes that questioned whether the current level of rates was restrictive enough.

Business activity measured by PMIs in the US accelerated driven by a strong improvement in the services sector (54.8 pts) taking the composite PMI reading to its highest in more than two years. Germany’s PMI readings were also robust (mfg 45.4, services 53.9) while Britain’s update came in mixed with a weaker services sector (52.9) than a month ago. Solid PMI readings discourage central banks from easing policy measures in the near term.

Turkey’s central bank kept its benchmark policy rate steady at 50% as expected on inflation concerns (70%) and signalled it plans to maintain then unch in the short term.

Japan’s core inflation slowed to 2.2% YoY in April from 2.6% in March, in line with forecasts, while headline inflation rose by 2.5%, also lower than a month ago, a sign that may delay the Bank of Japan’s plan to hike interest rates.

Asian markets are maintaining Wall Street’s negative sentiment with stocks in Australia, Hong Kong and Korea dropping by more than 1%, while Japan, Singapore and mainland China are lower by around 0.5%. European equity futures are also trading weaker with the FTSE falling 0.75%. However, S&P and Nasdaq futures are modestly firmer from last night’s close.

The US SEC has approved ETFs based on Ethereum, the second-largest cryptocurrency, and listed funds from Fidelity and Blackrock among others are expected to be launched soon. Ethereum (ETH) is firmer today at $3,800 while Bitcoin remains around $68k.

In corporate deals, British wealth manager Hargreaves Lansdown rejected a £4.7bn takeover approach by a consortium led by CVC and the Abu Dhabi Investment Authority stating it substantially undervalues its potential. Shares rallied 14% to the highest in two years and a market cap of £5.4bn. The co is trading at a trailing P/E ratio of 17.5x and has reported a profit every year since its 2007 listing on the LSE.

In business news, Ticketmaster parent, Live Nation Entertainment (LYV), saw shares drop 8% after being sued on antitrust grounds by the US Deparment of Justice which may lead to the break up of the ticketing company. Live Nation is valued at $23.5bn.

In IPOs, insurance company Bowhead Specialty Holdings (BOW) raised $128mn by listing on the NYSE at $17 and shares rallied 40% to close at $23.80 on its debut day, for a market value of ~$700mn. Founded in 2020, Bowhead is affiliated with American Family Insurance.

The IPO pipeline includes French optical equipment maker Exosens, formerly known as Photonis, which is planning to raise €180mn on Euronext and is controlled by private equity Groupe HLD.

It was an active day for euro-denominated corporate bond issuance and included senior notes by Phillips (8y @ ms+115, BBB+), Air Liquide (10y @ ms+62, A2), Hochtief (6y @ ms+142, BBB-), Mondi (8y @ Bunds+125, A-).

On the data front today, we’ll get retail sales in the UK, durable goods in the US, employment in Switzerland and PPI in Sweden.

That’s all for today, have a nice weekend.

Copyright © 2024 Laconic. All rights reserved. This publication, 'Markets Dawn Europe,' contains proprietary content and is intended solely for the recipient's personal use. Please share using the button below, as access is free to all.