Markets Dawn Europe: Fri 10 by 7AM UKT (8AM CET)

Brief Podcast 🎙 + Data 📊 + Script 📄

Script: Estimated reading time ⏲ ~4 mins

Good Friday,

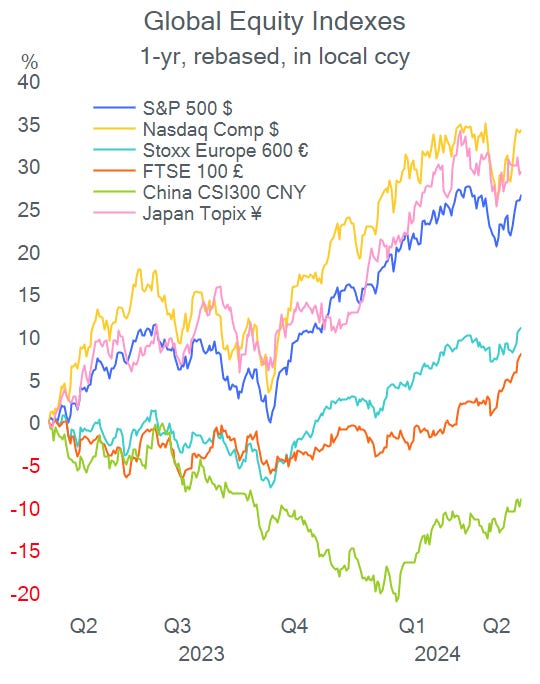

Equities on both sides of the Atlantic maintained their positive start of the month with the Stoxx 600, the FTSE and the Dax closing a new all-time highs. All leading US stock indices finished firmer last night with every sector in green except for information technology. The S&P 500 added 0.5%, with higher-than-expected weekly jobless claims as the key driver. Any indications of a cooling labor market further strengthen hopes for rate cuts. The next big data release in the US will be next week’s PPI and CPI inflation update.

In monetary policy, the Bank of England kept its base rate steady as widely anticipated at 5.25% with 2 (Ramsden and Dhingra) out of 7 voters opting for a rate cut to 5%. The central bank signalled that policy easing could start next month as it sees inflation dropping. Governor Bailey made some dovish remarks stating that rate reductions could be deeper than investors expect.

Cable ended modestly firmer at 1.2522 while 2-year yields fell 4bp to 4.28%, and the 10-year ended flat at 4.14%. Keep in mind that all three leading yield curves remain in inverted mode. The US yield curve shifted lower by 4bp yesterday while Bunds closed a touch higher.

Asian equities are trading firmer today with most indices up between 0.5-2%, and European futures are pointing to a positive open. Crude oil is also higher this morning, with Brent recovering the $84 mark.

Yesterday was a negative day for geopolitical conflicts in the Middle East and Russia.

-Israel dismissed Biden’s warning and proceeded to strike the city of Rafah in Gaza, as ceasefire talks ended with no deal and tensions escalated. Netanyahu claimed that Israel does not need Washington’s support.

-Putin made defiant remarks during Russia’s Victory Day military parade, referring to the use of nuclear weapons and stating that Moscow is ready to respond to any threat and is capable of striking any target in the world with missiles.

In the deals space, things got interesting in the Spanish banking sector. In a rare move, BBVA launched a hostile takeover attempt of smaller rival Banco Sabadell after the board rejected the initial friendly approach. BBVA submitted its all-share offer worth €12.2bn directly to shareholders, a move not well received by authorities. BBVA shares fell 7% while Sabadell gained 3% yesterday. BBVA offered 1 newly issued share for every 4.83 Sabadell shares, a premium of 30% to Sabadell’s undisturbed price which narrowed to 8% after BBVA shares declined. BBVA needs to get 50.1% acceptance from Sabadell’s shareholders as well as central bank approval.

South African shareholders of miner Anglo-American are open to an improved bid from BHP, which has until May 22 to formalize its £31bn takeover approach. Anglo closed 3% higher yesterday.

In IPOs, Florida-based Proficient Auto Logistics (PAL), a leading provider of transport in the auto industry, raised $215mn and was priced at $15. Shares fell marginally on their debut and closed at $14.75.

In economic updates today, we’ll get GDP, industrial and manufacturing output in the UK, and inflation in Norway and Denmark. There are no significant earnings releases scheduled for today.

Have a good weekend, see you on Monday.

Copyright © 2024 Laconic. All rights reserved. This publication, 'Markets Dawn Europe,' contains proprietary content and is intended solely for the recipient's personal use. Please share the publication using the button below, as access is free to all.